For many of us, cars are a necessity for everyday life, whether that’s commuting from work, going shopping or travelling the world. But what car do you choose to buy, and drive?

There are so many brands and so many retailers. And do you buy second hand or brand new? What colour - blue or green, or red, or one of the other numerous colours? Fancy leather seats? Any other upgrades and accessories?

There are so many different options that we rely heavily, not only on review sites, but also on the brands themselves, to tell us what we need to know to make an informed decision.

It comes down to marketing - marketing of the product and marketing of the brand.

There were an estimated 36.7m cars - according to gov.uk - on UK roads in 2016. That’s a staggering amount, showing how essential cars are in Britain and what a big opportunity there is for brands to capture. So, who’s really taking advantage of this opportunity and how are they doing it?

If you would like to see the strategy deck we created for this industry, then download it here >

Market Share

Firstly, to really know who’s capturing what and how they’re doing it, we really need to figure out who the ‘who’ is. To do that, I’ve taken the 100 most searched generic terms revolving around purchasing a car and removed all branded search including any specific models so I’m left with true generics such as ‘Buy a car’.

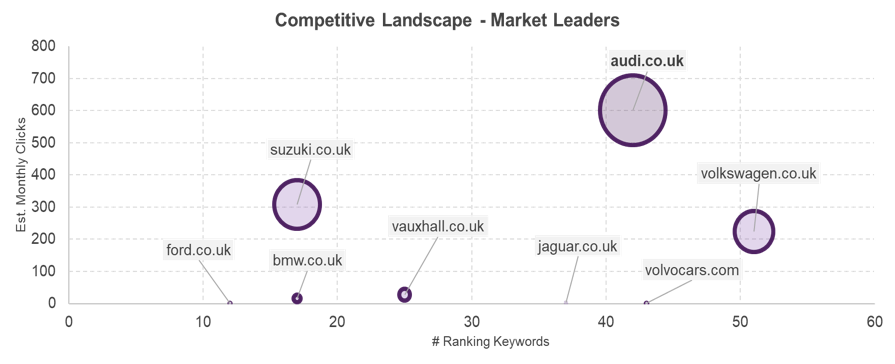

Then I have used an in-house scraping tool which reports back the top 10 SERPS for each keyword to see which brands are ranking the most in the highest positions. What I found was interesting. You can see below the market landscape with the better performing brands and you can do the same for your industry using this handy guide . Along the X axis is the number of keywords they rank for, with the Y axis reporting the estimated monthly clicks they’re getting. Effectively, the bigger the bubble the more visible you are with the optimum position being the top right-hand corner. This means you’re ranking for a lot of keywords in really good position.

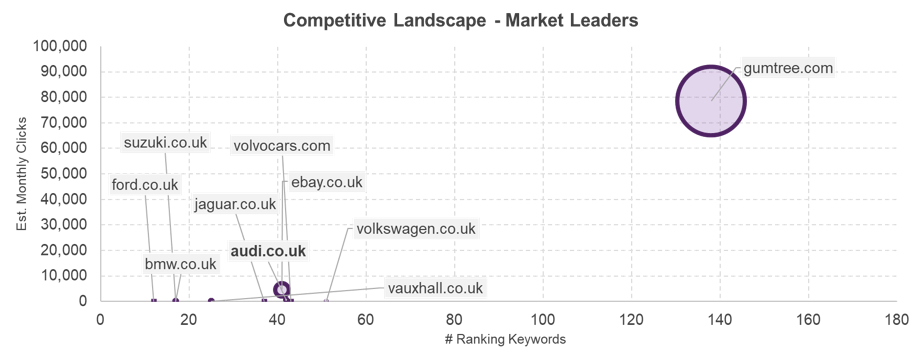

The first thing we can take from the graph is that out of 100 keywords, most brands rank for less than half, with the exception of Volkswagen, who rank for 51 terms. For reference below, I’ve put in the same chart but this time with generic car sale retailers that don’t specialise on brand. Suddenly the brands shrink significantly – with Gumtree having multiple pages ranking for multiple keywords.

Brand Awareness

This quite clearly demonstrates that, especially from an SEO perspective, brands aren’t targeting these generic terms. But if they’re not targeting them what are they targeting?

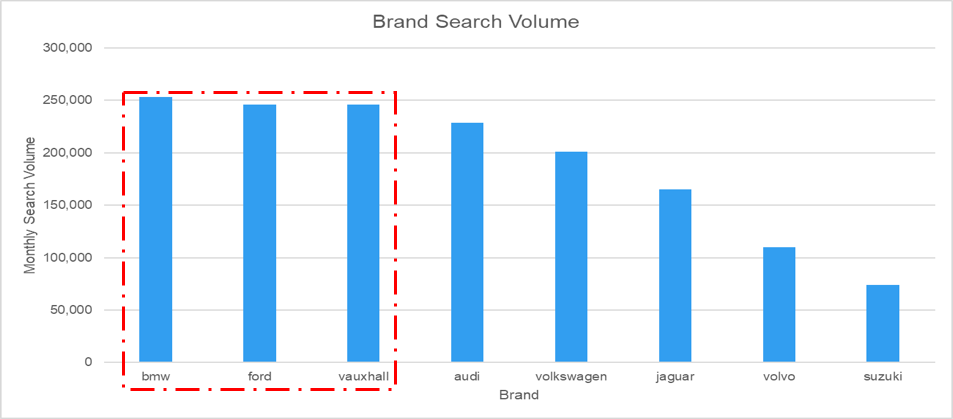

So, in an attempt to move away from generics and see what the brands are really focusing on, I ran a few reports based around monthly searches to see if anyone really stands out. Firstly, to see simply which brand was searched the most each month I ran search volumes through an in-house tool for each of our eight brands; just purely the brand name. Illustrated below are the results. I do have to point out a caveat at this point as I’m not naive to the fact that many people are car enthusiasts and not all searches are going to be transactional.

For example, BMW i8 has a search of 66k – although it’s an astonishing car it’s hard to believe all of these are transactional. They’re more likely to be people ogling over it and whispering, ‘one day’ to themselves.

This again, much like the market share bubble chart, didn’t really shed a lot of light or give any outright answer in relation to the most searched brand. Although yes BMW ‘won’ all the top three are within 6,000 of each other, which on this scale is pretty insignificant.

This step may not separate out who has more brand presence but what it does tell us is that it’s more important to ‘be a brand’ than to rank for the more generic terms. According to statistics from MarTech, 59% of shoppers prefer to buy new products from brands familiar to them which means we’re one step closer to understanding what they’re fighting over.

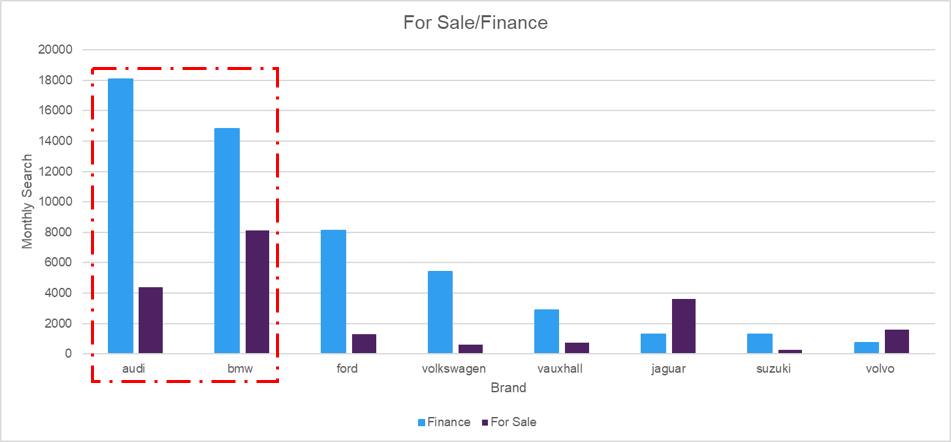

Continuing with the search volumes exercise I also took a number of common phrases and patterns that emerged:

- 'Brand' For sale

- 'Brand' Finance

By selecting these two terms we’re moving further down the purchase funnel. These are searches with transactional outcomes – whether that is directly transactional or eventually transactional with the searcher looking for price ranges. Hopefully this will give more of an idea as to which brand people are transactional towards.

This has revealed two clear leaders within the transactional query market, with BMW leading the way ‘for sale’ and Audi leading the way for ‘finance’ and them both being in second place in the other.

This means we’re getting somewhere with identifying the brand that’s most on people’s minds. Audi and BMW have got this tied up with regards to brand search – with both scores combined there isn't a competitor within 10,000 searches of them. There’s obviously a lot more to brand awareness than how many people search you a month, but this is the most tangible way of identifying any standouts.

We love a graph here at Zazzle Media - if you want to see more of this, then check out the strategy deck we crafted, and see the real tactics behind the winners and losers!

Proficiency

Here at Zazzle Media we develop strategies for a lot of clients that really delve into the strategic ranking aspects of our clients and their competitors.

We find out what’s doing well within the industry, and what, specifically, our client needs to do better to improve organically. With search now being more ‘multi-pronged’ than ever, we analyse many different metrics across the site.

We’ve learned that rather than thinking of each strategic aspect as separate entities we view them all as a linked machine, so we emphasise that working on one strategic aspect has an impact on the others. Just because we are building links this doesn’t mean we have forgotten about awareness.

I've developed a mini strategy revolving around these competitors viewing and analysing many of the aspects we would do for a client. Below are the results, which I’ll talk through below. For convenience, I’ve highlighted the ‘winner’ and ‘loser’ in each category with green and red.

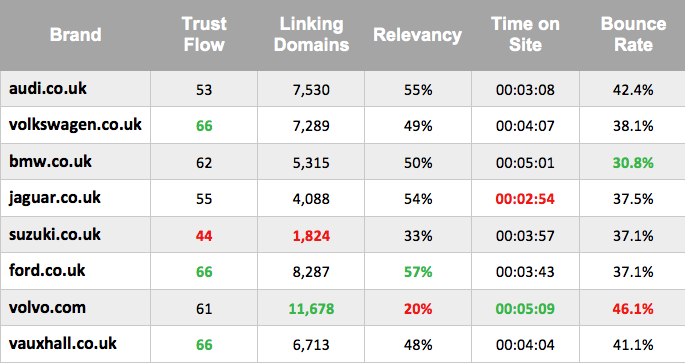

Backlink Profile

The first strategic aspect analysed was their back-link profiles. Highlighted in the green with the same trust flow are Volkswagen, Ford and Vauxhall, but interestingly the stand out by a significant amount of referring domains is neither of those three. It's Volvo.

This suggests that although Volvo has a lot of referring domains, some of them are lower quality, dragging the TF score down. With a TF of 61 they’re not really suffering from it so it’s more likely that the other three have very high quality referring domains which is pushing their TF up. So, in conclusion it's a bit of a mixed bag, but if pushed I would say Ford is the overall winner with the highest TF and the highest amount of referring domains out of the three tied on TF.

Relevancy

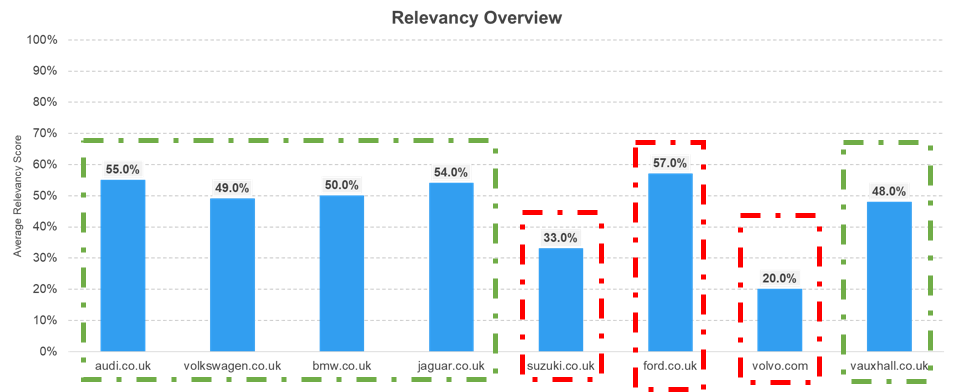

To determine on site relevancy, we have an in-house tool built that takes specified keywords and analyses the URLs of the site against those keywords to determine how well optimised the site is for the keywords. It then gives it a score out of 100%.

Anything between 60%-70% we, as a rule of thumb, accept as ‘optimal’. Anything under is classed as being under-optimised and anything over it over-optimised. Obviously, it being a rule of thumb, there are exceptions. We generally take a medium of the industry to determine where ‘optimal’ is as it may not always be 60%-70%.

Under optimised can be an issue due to Google struggling to even identify that the URL is targeting that keyword, hence rankings can be poor. Over optimised is also an issue as sometimes Google can see it as ‘keyword stuffing’ and spammy, thinking a site is using old school SEO tactics to outsmart it and again rankings can be poor – making it even more important to hit that optimal spot.

Drawing back to our automotive industry, I’ve run relevancy for singular keywords ‘brand for sale’ across the whole site. From this, we can identify that the optimal 10% difference is between 45% - 55%. This means we have five that would be ‘optimal’, two under optimised and one over optimised. Statistically speaking, BMW would be categorised as effectively ‘optimal of the optimal’ as they’re bang in the middle of the 10% range, but really any optimal score is functionally relevant. Again, this time we have a few contenders of who ‘won’ this strategic aspect.

Engagement

Engagement metrics are something we normally consider when developing a strategy, especially if it’s a content heavy brief or the client is performing particularly badly in comparison to the industry.

As with all strategic aspects, we apply some more heavily to specific industries using discretion. Although I have measured engagement metrics for the sake of this piece, it doesn’t appear that engagement is an important aspect for this industry.

All the metrics are particularly low, but looking further into this, none of the sites appear to have a specific blog attached to their site, with very minimal content also located on the site in any capacity. Informational content is a heavy driver of traffic towards sites, especially through organic, so there are two ways you could possibly view this – either the industry leaders don’t suit this particular content, mostly due to people generally looking for impartial advice and answers, or it’s an opportunity to explore that no one else has.

Generally, I'm leaning more towards to the first statement. The traffic towards sites such as WHAT CAR and Auto Express is extremely high and that’s mostly due to their free, impartial advice and reviews. Competing with giants such as this wouldn’t be a beneficial use of time, resources or spend.

It’s All About the People

Marketing is all about the people. If you’re not appealing to your target audience in the right ways to reach them, then it doesn’t matter how good you are at what you do, people aren’t going to know about it. We don’t only develop personas here at Zazzle Media, we develop them one step further and associate them to micro moments and pain points so we can really understand our target audience. It’s important to understand who they are, what they want and how they want it given to them - especially on an ecommerce site.

I’ve looked at all the brands' sites to really get a feel of how the user experience is. Now, it goes without saying that I’m not about to buy eight brand new cars to get a full buying user experience, but I’ll do my best to simulate it as far as possible.

I decided to spend a little time browsing the site, using the navigation bar, main menu, drop down bars, etc, and then I’ll go back to the homepage and attempt to buy my own most popular model, with a few customisations. I decided to attempt customising with built in Satellite navigation and Bluetooth – two generally standard extras in today’s market. This will give a good feel as to how easy the buying experience is to a particular specification.

The Experience

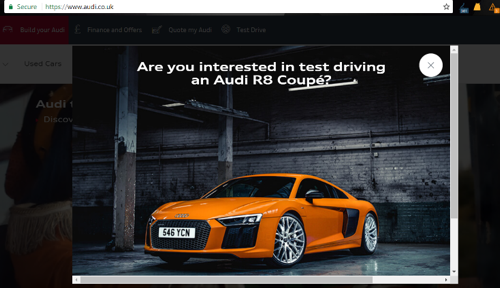

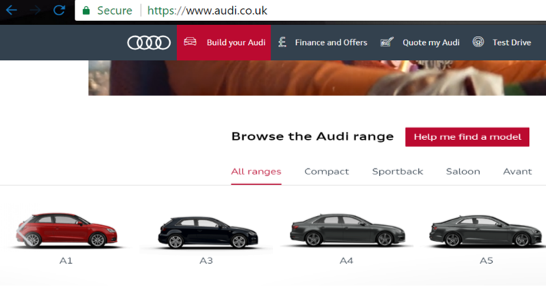

Once ogled out - I managed to divert myself away from the Audi R8 pop out Audi greeted me with – I found it a very sophisticated site to use, very clean, very obvious and overall, very customer focused. On the homepage, you’re welcomed with a selection of their models displayed by picture so even if you’re not sure of the model you can select the car you’re thinking of/want.

I clicked through to Audi A1 and start to search for my upgrades. First of all, you’re met with a swarm of information which can be intimidating, but once you’ve processed the information there’s a convenient ‘build your Audi’ button which takes you through step by step in selecting every aspect of your Audi, including any upgrades along the way.

So overall, it's a very simple process. From the home page, it's less than ten clicks and you have a personalised Audi with an estimated price, which is incredible efficiency for such a complex purchase.

Volkswagen have a very similar experience to Audi. A video takes over your screen at the top of the page showing you all the ‘cool’ features their cars have. In contrast to Audi, Volkswagen have a very similar model toolbar, but it’s located below the fold and you have to scroll past the video to see it. It would be interesting to see the effect that has on CTR in comparison to Audi.

Although the build your own car experience is very similar, it's not quite so easy to locate it. Below the fold significantly is a tool bar right at the very bottom which has a build your own option. I later discovered, after firing the mouse around the page, that there’s a quick access toolbar. This is a great feature, but it assumes you know what the bar is there for. Once hovered over, each widget reveals more details, but before that it’s almost just a floating bar that looks out of place.

BMW, in contrast, is different. No flashy video, no interactive picture loaded toolbar, just a slideshow of images - one of which is ‘build your BMW online’. Considering BMW would generally be classified as one of the upper middle tier brands, the site feels very different and low key especially in comparison to Audi and Volkswagen. It doesn’t feel as smooth or as easy.

Attempting to customise your selected model takes a considerable amount of time clicking around disguised buttons and dodging the ‘find your local dealer’ options. The impression is that BMW would rather that you experience BMW from within a showroom than online. It feels very rigid and clunky rather than customer focused. Volvo and Vauxhall are very similar. There’s very little interactivity, and very little enticement apart from a picture greeting you on the home page with a couple of attractive pictures.

I’ve grouped Ford and Suzuki together as they’re very similar sites in many aspects. The main page is dominated by big aspects with images and videos and very obvious calls to actions up and down the pages. Although there is a task bar on the Ford site similar to the Volkswagen task bar, Ford actually pre-load the options out. Once you scroll it cascades into a smaller taskbar with just the images. This is a good piece of functionality as now you know what the options are and the fact that it is actually a navigation bar doesn’t confuse you. The process of customising your options is the same on both sites with very little to confuse you but also very little to excite you. It’s simple and straight forward but lacks engagement and excitement.

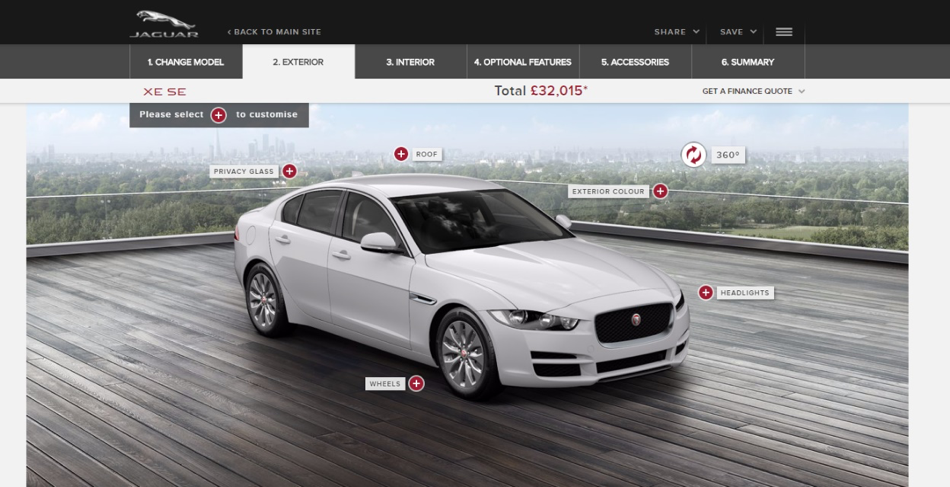

Jaguar feels almost a carbon copy of Audi’s website, which isn’t a bad thing. It’s very smooth and similarly clean and obvious. The build experience is really something special. You build your own Jaguar in front of your very eyes, down to the most minute details. This is heavily in contrast to BMW, which feels like they want to get you away from the site. By far the website to beat, it’s so simple yet so effective.

Who’s the Real Winner?

Proficiency Review

So, I’ve now completed a data strategy review of the eight sites. What that now means is we can take a step back and look at who’s got the edge overall. We quickly found out that specific brands weren’t focusing upon generic car sale terms. This was well illustrated by the market share graphs, which showed that in comparison to sellers that sold many different brands (usually second hand) our brands really didn’t have a leg to stand on.

This showed us that brands heavily rely on brand awareness and people either directly coming to them or branded organic traffic, so I set out to find out who owned this strategic aspect.

The results were close with two companies coming out on top of the brand awareness ladder; Audi and BMW were within 400 searches of each other and over 13,000 above everyone else.

In terms of backlink profile, we have three companies leading the way in trust flow – Volkswagen, Ford and Vauxhall. Out of those three, Ford had the most number of backlinks.

In terms of relevancy all competitors were pretty similar – there’s no out and out winner of this aspect as many where within the optimised range. Engagement was decided as not relevant in this industry with no competitors showing any strong metrics. In terms of UX, Jaguar were a very clear winner with easily the most user friendly, attractive UI. Which leaves us with these:

The Winner

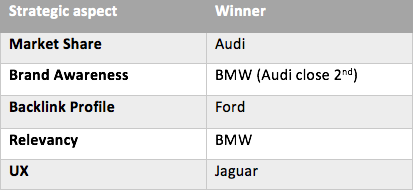

As we can all see from the table above, we’ve got a list of strategic winners and BMW coming out on top of two aspects.

In some cases, this would mean that BMW is the winner, but not in this test. What I discovered early on in this piece is that the auto industry fell back on one of the main marketing principles. It’s all about the people. The digital auto industry is all based around brand awareness and user experience, as purely organic results don’t appear that important, people need to know who you are and what you do.

Once brand awareness is down, branded organic will be coming through to the site, so once they’re there it’s important to keep them there. Our winners of the brand awareness were BMW with Audi as a very close second. This, coupled with Audi’s win of the ‘generic market share’, puts them in pole position.

The next important part is UX and although Jaguar won this by a considerable amount they barely featured in our brand awareness section. Audi have a beautiful UI which is simple, effective and direct, whereas BMW looks clunky, awkward and feels as if they’d prefer you in a showroom than on their site. Audi also have a reasonably strong backlink profile and meet the relevancy requirements for the industry.

So there we have it - the overall winner of the automotive industry for putting people first, and making sure their audience know who they are, is... Audi.

Don't forget to download the strategy deck we created for the auto industry - to show what we would be aiming for in this market!

If you have any questions about this investigation please get in touch here!

Stay in touch with the Zazzle Media family

Sign up for our monthly newsletter and follow us on social media for the latest news.